Aerospace & Defense Power Connector Market Overview - Definition, scope, and significance?

The Aerospace & Defense Power Connector market comprises specialized electrical connectors that transmit power within aircraft, missiles, satellites, naval vessels, and ground‑based military platforms. These connectors must meet stringent standards for reliability, vibration resistance, temperature extremes, and mission‑critical performance. The market’s scope covers design, manufacturing, testing, and aftermarket support for connectors ranging from low‑current (5 A) to high‑current (> 900 A) applications, serving both commercial aerospace and defense sectors. Their significance lies in enabling safe, efficient power distribution for avionics, weapon systems, and mission‑essential equipment, directly influencing vehicle uptime and operational readiness.

Aerospace & Defense Power Connector Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising defense spending, accelerated commercial aircraft fleet renewal, and the proliferation of electric propulsion and unmanned systems that demand higher‑current, lightweight connectors. Technological advances such as miniaturization and smart‑connector diagnostics also stimulate demand. Restraints stem from stringent certification processes, long product development cycles, and the high cost of aerospace‑grade materials. Challenges involve supply‑chain disruptions and the need for compliance with multiple international standards. Opportunities arise from emerging markets investing in modern air forces, the growth of hypersonic programs, and the shift toward modular, plug‑and‑play connector architectures.

Aerospace & Defense Power Connector Market Growth Trends - Current and emerging trends shaping the market?

Current trends include the migration from circular to rectangular connector designs to maximize payload density, and a focus on lightweight composites to reduce overall aircraft weight. Manufacturers are integrating sensor‑embedded contacts for real‑time health monitoring. Emerging trends feature the adoption of high‑temperature silicon‑carbide (SiC) materials for next‑generation propulsion, and the development of high‑power (> 300 A) connectors to support electric taxi and hybrid‑electric aircraft concepts. Additionally, there is a growing preference for standardized connector families across multiple platforms to simplify logistics.

COVID-19 Impact on the Aerospace & Defense Power Connector Market - Pandemic effects and recovery trajectory?

The pandemic caused a temporary dip in commercial aircraft production, leading to reduced short‑term orders for power connectors. Defense programs, however, remained largely insulated due to government commitments, cushioning the impact. Supply‑chain bottlenecks for critical raw materials delayed some projects, but accelerated digital collaboration tools helped mitigate design delays. Recovery is now evident as airlines resume fleet modernization and defense budgets rebound, positioning the market on a steady growth path aligned with the projected 5.29 % CAGR.

Aerospace & Defense Power Connector Market Competitive Landscape - Major competitors and market consolidation?

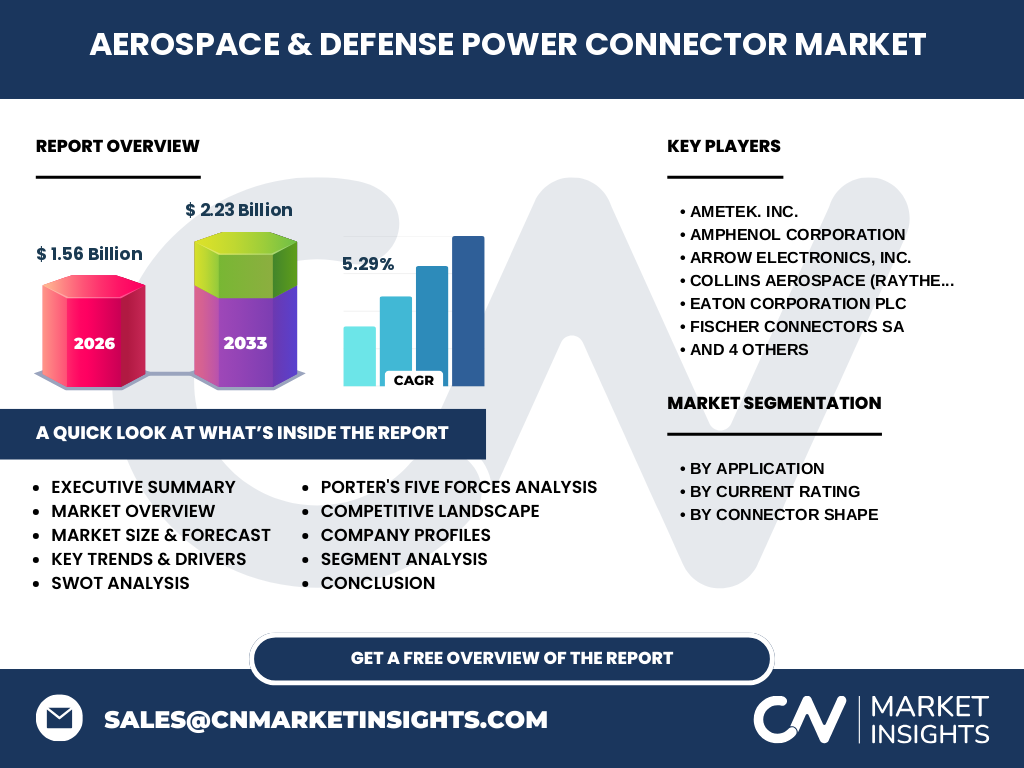

The competitive arena is dominated by established OEMs such as AMETEK, Inc., Amphenol Corporation, Arrow Electronics, Inc., Collins Aerospace (Raytheon Technologies), Eaton Corporation plc, Fischer Connectors SA, ITT Corporation, Molex, LLC, Radiall, and TE Connectivity. These firms compete on engineering expertise, product breadth, and global service networks. Recent consolidation includes strategic acquisitions aimed at expanding high‑current connector portfolios and strengthening presence in emerging defense markets, fostering a more integrated value chain.

Executive Summary - High-level overview and key findings about Aerospace & Defense Power Connector Market?

The Aerospace & Defense Power Connector market is valued at $1.56 billion in 2026 and is projected to reach $2.23 billion by 2033, reflecting a 5.29 % CAGR. Growth is propelled by rising defense expenditures, electric propulsion trends, and the need for reliable high‑current solutions. While certification and supply‑chain complexities pose challenges, opportunities in modular designs and smart‑connector technologies promise additional revenue streams. The market is concentrated among a few global players who are pursuing acquisitions and product innovation to capture expanding demand.

Aerospace & Defense Power Connector Market Forecast - Projections for 2025-2032 period?

Based on current trends and the provided CAGR, the market is expected to expand from approximately $1.48 billion in 2025 to $2.10 billion by 2032, maintaining steady growth each year. High‑current (> 300 A) segments will exhibit the fastest expansion, driven by electric and hybrid propulsion initiatives. Regional growth will be strongest in North America and Europe due to mature defense programs, while Asia‑Pacific will accelerate as governments increase aerospace capabilities.

Aerospace & Defense Power Connector Market Size and Share by Segmentation - Breakdown by segment?

By application, the market divides into Aerospace, Military Ground Vehicle, Body‑worn Equipment, and Naval Ships, each requiring distinct current ratings and form factors. By current rating, categories span from 5‑40 A up to > 600‑900 A, with higher‑current brackets gaining market share as electric power demands rise. By connector shape, rectangular and circular forms compete, with rectangular units growing faster due to space‑efficiency trends in modern airframes.

Global Aerospace & Defense Power Connector Market Size and Share by Region - Geographic distribution?

The market’s global footprint is anchored in North America, Europe, and the Asia‑Pacific. North America leads in defense spending and hosts major OEM headquarters, contributing the largest revenue slice. Europe follows, driven by extensive commercial aviation activity and NATO procurement. Asia‑Pacific shows the highest growth potential, reflecting rapid defense modernization programs and expanding commercial aircraft orders in China and India.

Regional Analysis of the Aerospace & Defense Power Connector Market - Detailed regional market performance?

In North America, demand is fueled by continuous upgrades to fighter fleets and the rollout of next‑generation commercial jets. Europe’s market benefits from stringent certification regimes that encourage high‑quality connector solutions, alongside strong naval shipbuilding programs. The Asia‑Pacific region experiences accelerated growth due to increased military budgets, a surge in indigenous aircraft development, and the establishment of new aerospace manufacturing hubs. Middle‑East markets, while smaller, are investing heavily in defense infrastructure, presenting niche opportunities.

Leading Company Profiles in the Aerospace & Defense Power Connector Market - Industry players and strategies?

AMETEK, Inc. focuses on high‑reliability connectors for critical defense platforms, leveraging its advanced materials expertise. Amphenol Corporation expands its product line through strategic acquisitions targeting high‑current segments. Arrow Electronics, Inc. emphasizes supply‑chain integration and aftermarket services. Collins Aerospace (Raytheon Technologies) invests heavily in smart‑connector technologies and digital twins. Eaton Corporation plc capitalizes on its power‑management portfolio to offer turnkey connector solutions. Fischer Connectors SA, ITT Corporation, Molex, LLC, Radiall, and TE Connectivity each pursue innovation in miniaturization, ruggedization, and global distribution networks.

Porter's Five Forces Analysis of the Aerospace & Defense Power Connector Market - Competitive forces assessment?

Threat of new entrants is low due to high entry barriers like certification costs and specialized tooling. Bargaining power of suppliers is moderate; while raw‑material suppliers of aerospace‑grade alloys hold some leverage, large manufacturers often negotiate long‑term contracts. Bargaining power of buyers is strong, especially defense agencies that demand strict compliance and volume pricing. Threat of substitutes remains limited because few alternatives meet the same reliability standards. Industry rivalry is high, with several global players competing on technology, lead time, and lifecycle support.

SWOT Analysis of the Aerospace & Defense Power Connector Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established OEM capabilities, high entry barriers, and critical role in mission‑essential systems. Weaknesses: Long development cycles and dependence on limited high‑grade material sources. Opportunities: Growth of electric propulsion, smart‑connector diagnostics, and modular platform adoption. Threats: Geopolitical trade restrictions, potential supply‑chain shocks, and rapid technology shifts that could render legacy designs obsolete.

Aerospace & Defense Power Connector Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw‑material sourcing (high‑grade copper, titanium, composites), followed by precision engineering and tooling, component manufacturing, rigorous testing & certification, and finally integration into OEM platforms. After‑market services, including repair, refurbishment, and lifecycle support, add recurring revenue. Strategic partnerships between material suppliers and connector manufacturers help streamline the chain, while digital twins and simulation tools reduce time‑to‑market.

Key Investment Insights in the Aerospace & Defense Power Connector Market - Strategic investment recommendations?

Investors should target companies with strong defense contracts and proven high‑current connector portfolios, as these segments are projected to outpace overall growth. Funding R&D in smart‑connector and sensor integration offers high upside given the industry’s move toward predictive maintenance. Acquisitions of niche firms specializing in lightweight composites can accelerate entry into electric‑propulsion markets. Finally, focusing on Asia‑Pacific expansion through joint ventures can capture the fastest‑growing demand base.

Aerospace & Defense Power Connector Market Conclusion - Summary and key takeaways?

The market is on a robust growth trajectory, moving from a $1.56 billion base in 2026 to $2.23 billion by 2033, underpinned by a 5.29 % CAGR. Drivers such as defense spending, electric aircraft, and high‑current needs outweigh the constraints of certification and supply‑chain complexity. Leading OEMs are consolidating and innovating, creating a competitive yet opportunity‑rich environment. Prospects remain strongest for high‑power, smart‑enabled connectors and for expansion in the Asia‑Pacific region.

Research Methodology - How this research was conducted?

The study combines primary interviews with industry engineers, procurement officers, and defense analysts, plus secondary analysis of publicly available financial reports, regulatory filings, and market databases. Data triangulation ensures accuracy, while forecasting utilizes the disclosed CAGR of 5.29 % applied to the 2026 baseline of $1.56 billion. Competitive mapping draws from company press releases, product catalogs, and merger‑acquisition announcements.

Research Scope - Coverage and limitations?

The scope encompasses all power connectors used in aerospace and defense platforms, segmented by application, current rating, and connector shape. Geographic coverage includes major markets in North America, Europe, and Asia‑Pacific. The analysis excludes unrelated consumer‑grade connectors and does not quantify proprietary defense program spend beyond publicly disclosed figures.

Key Companies and Recent Developments in the Aerospace & Defense Power Connector Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent highlights include AMETEK’s launch of a new high‑temperature connector line for hypersonic vehicles, Amphenol’s acquisition of a niche high‑current connector maker to broaden its > 300 A portfolio, and Collins Aerospace’s partnership with a leading electric‑propulsion startup to co‑develop lightweight rectangular connectors. TE Connectivity announced a smart‑connector platform with embedded health‑monitoring sensors, while Molex unveiled a modular connector system aimed at simplifying logistics for naval ship retrofits. These activities illustrate a market moving toward higher performance, intelligence, and integration.